Journal

What is an Event

An Event is any happening or occurrence in the life of a business. It can be internal or external.

Key Characteristics:

-

It is a happening.

-

It may or may not involve money.

-

It may or may not change the financial position of the business.

-

Not recorded in the books of accounts.

What is a Transaction

A Transaction is a specific type of event. It is an economic event that involves a transfer of money or money’s worth (goods, services, assets) between two parties or within the business.

Key Characteristics:

-

It is a happening (an event).

-

It involves value (money or money’s worth).

-

It brings about a change in the financial position (Assets, Liabilities, or Capital).

-

It is recorded in the books of accounts (Journal, Ledger, etc.).

For a transaction to occur, two conditions must be met:

-

Monetary Value: It must be measurable in terms of money.

-

Dual Aspect: It must have two effects (e.g., something comes in, something goes out; or one account is debited, another is credited). This is the basis of the Dual Aspect Concept.

Differences: Transaction vs. Event

| Basis | Transaction | Event |

|---|---|---|

| Meaning | An exchange of goods, services, or assets for money or promise of money. | Any happening or occurrence in the business. |

| Monetary Value | Always measurable in monetary terms. | May or may not be measurable in money. |

| Change in Financial Position | Always changes the financial position (Assets, Liabilities, Capital). | May or may not change the financial position. |

| Recording | Recorded in the books of accounts. | Not recorded in the books of accounts (unless it becomes a transaction). |

| Example | Purchased goods for ₹10,000. | Death of a key employee. |

What is a Journal

The word “Journal” comes from the French word “Jour,” which means day.

A Journal is the book of original entry (also called the book of prime entry or day book). It is the first place where a transaction is recorded in the books of accounts.

Think of it as the diary of a business. Just as you write down a significant event in your personal diary on the day it happens, a business records its financial transactions in the Journal on the day they occur, in chronological order (date-wise).

The Format of a Journal

A journal has a specific format with five columns.

| Date | Particulars | L.F. | Debit Amount (₹) | Credit Amount (₹) |

|---|---|---|---|---|

| Date | Account to be Debited (Name) Dr. | XX | ||

| Account to be Credited (Name) | XX | |||

| (Explanation/Narration) |

How to Journalize (The Process)

Journalizing is the process of recording a transaction in the Journal. To journalize correctly, you must follow the Golden Rules of Accounting based on the type of account.

The Double Entry System is a scientific and complete system of recording financial transactions. It is based on the principle that every transaction has two aspects (a dual effect).

The Core Principle:

Every transaction affects at least two accounts. One account receives the benefit (Debit), and the other gives the benefit (Credit). For every transaction, the total amount debited must always equal the total amount credited.

“For every Debit, there is a corresponding and equal Credit.”

This system ensures the Accounting Equation always balances:

Assets = Liabilities + Capital

Basically there are two approach of passing journal entry

- Traditional Approach

- Modern Approach

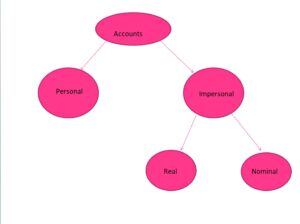

Traditional Approach

the classification of accounts is divided into Personal Accounts and Impersonal Accounts. Non-personal accounts are technically called Impersonal Accounts.

An Impersonal Account is any account that is not related to a natural person, artificial person, or representative person.

The Three Golden Rules of Accounting

Account Type Golden Rule Meaning Personal Account Debit the Receiver,

Credit the Giver.When a person or entity receives something from the business, their account is debited. When a person or entity gives something to the business, their account is credited. Real Account

(Non-Personal)Debit what comes in,

Credit what goes out.When an asset (like cash, machinery, or goods) enters the business, it is debited. When an asset leaves the business, it is credited. Nominal Account

(Non-Personal)Debit all expenses and losses,

Credit all incomes and gains.All costs incurred (expenses) or value lost are debited. All revenue earned (incomes) or value gained are credited.